Basic Economic Concepts

Economics is all about how people, businesses, and governments make choices about using limited resources — like money, time, or materials — to meet their needs and wants. Let’s look at the key concepts one by one:

1. Needs and Wants

- Needs are things we must have to live — like food, water, shelter, and clothing.

- Wants are things we’d like to have, but we don’t need to survive — like video games, snacks, or fancy clothes.

In economics, people must choose what to spend money on, because we can’t have everything.

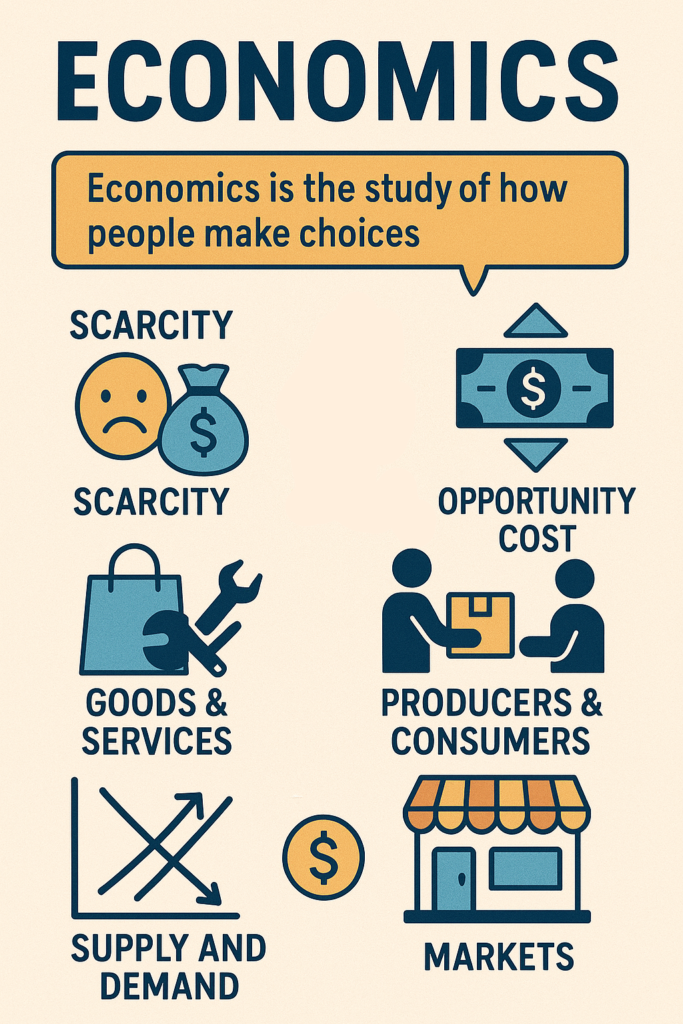

2. Scarcity

- Scarcity means there’s not enough of something for everyone.

- For example, there’s only so much land, water, money, and time.

Because of scarcity, people must make choices — and that’s what economics is all about.

3. Opportunity Cost

- When you choose one thing, you give up another.

- The opportunity cost is the next best thing you didn’t choose.

Example: If you buy a toy instead of a book, the book is your opportunity cost.

4. Goods and Services

- Goods are physical items you can buy and touch — like toys, food, or clothes.

- Services are actions people do for others — like haircuts, teaching, or fixing cars.

People buy goods and services to satisfy their needs and wants.

5. Producers and Consumers

- Producers are people or businesses that make or provide goods and services.

- Consumers are the ones who buy and use them.

Example: A bakery is a producer. You, buying a cupcake, are a consumer.

6. Supply and Demand

- Supply is how much of something is available.

- Demand is how much people want it.

When something is in high demand but there’s low supply, the price goes up. If supply is high and demand is low, prices go down.

7. Market and Price

- A market is where buyers and sellers come together (in person or online).

- Price is how much something costs, based on supply and demand.

Prices help decide what gets made and who gets it.

8. Money and Trade

- People use money to buy goods and services.

- Trade means exchanging things, either with money or by bartering (trading one item for another).

Example: You give $10 to buy a toy = trade using money. Or trade your snack for your friend’s pen = bartering.

Summary:

Economics is the study of how people make choices because resources like money, time, and goods are limited. We all have needs and wants, but because of scarcity, we can’t have everything. So, we must decide what to spend or use, which leads to opportunity cost — the thing we give up. People buy goods (items) and services (actions), and the people who make them are called producers, while buyers are consumers. The prices of things depend on supply and demand. All of this happens in markets, where trade and money help people exchange what they need and want. These basic economic ideas help us understand how the world works and how we all make choices every day.

Tags: bartering, buying, choice, consumers, consumption, cost, demand, economic behavior., economic decisions, economic systems, Economics, exchange, Financial literacy, goods, limited resources, market, money, needs, opportunity cost, price, producers, production, resource allocation, scarcity, selling, services, supply, trade, value, wants